California Resources Corporation Announces Fourth Quarter 2018 and Full Year Results

Business Wire 27-Feb-2019 4:15 PM

California Resources Corporation (NYSE:CRC), an independent

California-based oil and gas exploration and production company, today

reported net income attributable to common stock (CRC net income) of

$346 million, or $7.00 per diluted share, for the fourth quarter of

2018. Adjusted net income1 for the fourth quarter of 2018 was

$26 million, or $0.53 per diluted share. For the full year of 2018, CRC

net income was $328 million, or $6.77 per diluted share. Adjusted net

income1 for the full year of 2018 was $61 million, or $1.27

per diluted share.

This press release features multimedia. View the full release here:

https://www.businesswire.com/news/home/20190227005941/en/

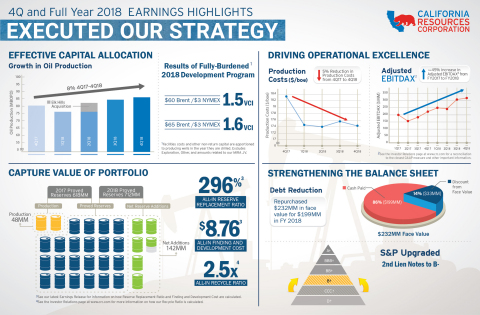

4Q and Full Year CRC Earnings Infographic (Graphic: Business Wire)

Adjusted EBITDAX1 for the fourth quarter of 2018 was $314

million and $1,117 million for the full year of 2018. Cash provided by

operating activities was $68 million for the fourth quarter of 2018 and

$461 million for the full year of 2018, or an 86% increase over the full

year $248 million in 2017.

Quarterly Highlights

-

Produced an average of 136,000 barrels of oil equivalent (BOE) per

day, an increase of 8% over the prior year period

-

Produced an average of 86,000 barrels of oil per day, an increase of

8% over the prior year period

-

Generated core adjusted EBITDAX1 of $352 million, which

excludes $50 million of net settlement payments on commodity

derivative contracts offset by $12 million related to cash-settled

stock-based compensation

-

Reported adjusted EBITDAX1 of $314 million and an adjusted

EBITDAX margin1 of 41%

-

Invested $197 million of total capital, including internally funded

capital of $174 million with the remainder funded by joint venture

(JV) partners

-

Drilled 86 wells with internally funded capital and five wells with JV

capital

Full Year Highlights

-

Produced an average of 132,000 BOE per day, an increase of 2% over the

prior year

-

Generated core adjusted EBITDAX1 of $1,374 million, which

excludes $228 million of net settlement payments on commodity

derivative contracts and $29 million related to cash-settled

stock-based compensation

-

Reported adjusted EBITDAX1 of $1,117 million and an

adjusted EBITDAX margin1 of 39%

-

Invested $747 million of total capital, including internally funded

capital of $641 million with the remainder funded by JV partners

-

Drilled 237 wells with internally funded capital and 106 wells with JV

capital

-

Implemented $34 million of annualized synergies in the nine months

following the Elk Hills acquisition, significantly exceeding the

initial target of $20 million in a shorter time frame than expected

Todd A. Stevens, CRC's President and Chief Executive Officer, said, "In

2018, our strategic approach focused on capturing the full value of our

portfolio, driving operational excellence, efficiently and effectively

allocating capital, and strengthening the balance sheet. We made good

progress on each priority, increasing the impact of our investment

program and delivering 8% growth in oil production from the fourth

quarter of 2017 to the fourth quarter of 2018. We invested in

value-driven activity to develop our core and growth areas with the

support of strategic JV capital, in addition to successfully resuming

our exploration program. We also harnessed our operating expertise to

generate more synergies than expected around the consolidation of our

flagship Elk Hills asset. We are entering 2019 with a internally funded

capital program of $300 to $385 million, which we will adjust to align

our financial and operating plans to market conditions. We are also in

discussions to obtain additional investments from new and existing JV

partners that could increase our capital program by $100-$150 million to

support a total capital budget of approximately $500 million. This will

allow us to maintain activity and efficiency gains, while retaining a

high degree of operational flexibility. Supported by our diverse asset

base, high level of operating control and dynamic business model, we

expect to continue to deliver meaningful value for our shareholders in

2019 and beyond."

Fourth Quarter 2018 Results

For the fourth quarter of 2018, CRC net income was $346 million, or

$7.00 per diluted share, compared to a net loss attributable to common

stock (CRC net loss) of $138 million, or $3.23 per diluted share for the

same period of 2017. Adjusted net income1 for the fourth

quarter of 2018 was $26 million, or $0.53 per diluted share, compared

with an adjusted net loss1 of $14 million, or $0.33 per

diluted share for the same prior year period. The 2018 results reflected

increased production and higher realized commodity prices for oil and

natural gas compared to 2017. The fourth quarter of 2018 adjusted net

income1 excluded $295 million of non-cash derivative gains on

commodity contracts, a $6 million non-cash derivative loss from

interest-rate contracts and a net gain of $31 million on debt

repurchases.

Total daily production volumes averaged 136,000 BOE per day for the

fourth quarter of 2018, compared to 126,000 BOE per day for the fourth

quarter of 2017, an increase of 8%, largely driven by the Elk Hills

acquisition in the second quarter of 2018. For the fourth quarter of

2018, oil volumes averaged 86,000 barrels per day, NGL volumes averaged

16,000 barrels per day and gas volumes averaged 204,000 thousand cubic

feet (MCF) per day. Organically, oil production grew over 1,000 barrels

per day from the third quarter of 2018 to the fourth quarter of 2018,

excluding the effects of production sharing-type contracts (PSCs) and

acquisitions.

Realized crude oil prices, including the effect of settled hedges,

increased by $3.05 per barrel for the fourth quarter of 2018 to $59.97

per barrel from the same prior year period. Settled hedges decreased

realized crude oil prices by $6.15 per barrel for the fourth quarter of

2018. Average realized NGL prices registered $43.56 per barrel,

reflecting a realized price that was 64% of Brent prices. Realized

natural gas prices were $3.77 per MCF for the fourth quarter of 2018,

$1.00 higher than the same prior year period. The increase in realized

gas prices resulted from the effects of limited third-party storage and

pipeline constraints.

Production costs for the fourth quarter of 2018 were $233 million, or

$18.61 per BOE, compared to $227 million, or $19.64 per BOE, for the

fourth quarter of 2017. In line with industry practice for reporting

PSCs, CRC reports gross field operating costs, but only CRC's share of

production volumes, which results in higher production costs per barrel.

Excluding this PSC effect, per unit production costs1 for the

fourth quarter of 2018 would have been $17.44 per BOE compared to $18.31

for the same prior year period. The decrease in production costs per BOE

was primarily driven by higher production between comparative periods,

largely related to the Elk Hills acquisition. Elk Hills' production

costs are lower than the average CRC-wide production cost per barrel. As

a result, the Elk Hills acquisition had a favorable effect on production

cost per barrel. General and administrative expenses (G&A) were $65

million for the fourth quarter of 2018 compared to $66 million for the

prior year period.

CRC reported taxes other than on income of $29 million for the fourth

quarter of 2018 compared to $33 million for the same prior year period.

Exploration expense was $16 million for the fourth quarter of 2018, $11

million higher than the same prior year period due to exploration dry

holes.

CRC's internally funded capital investment for the fourth quarter of

2018 totaled $174 million, of which $119 million was directed to

drilling and capital workovers. CRC's JV partner Benefit Street Partners

LLC (BSP) funded $12 million, which is included in CRC's consolidated

results, while JV partner Macquarie Infrastructure and Real Assets Inc.

(MIRA) funded an additional $11 million of investment, which is excluded

from our consolidated results.

Cash provided by operating activities was $68 million for the fourth

quarter of 2018, which included interest payments of $157 million.

Full Year 2018 Results

For the full year of 2018, CRC net income was $328 million, or $6.77 per

diluted share, compared to a CRC net loss of $266 million, or $6.26 per

diluted share, for the full year of 2017. Adjusted net income1

for 2018 was $61 million, or $1.27 per diluted share, compared with an

adjusted net loss1 of $187 million, or $4.40 per diluted

share, for 2017. The 2018 results reflected significantly higher

realized prices and higher production, partially offset by increased

production costs, as well as higher G&A and interest expense. The 2018

adjusted net income1 excluded $224 million of non-cash

derivative gains on commodity contracts, a net gain of $57 million on

debt repurchases, a $6 million non-cash derivative loss from interest

rate contracts, a $5 million gain on asset divestitures and a net $13

million charge related to other unusual and infrequent items. The 2017

adjusted net loss1 excluded $78 million of non-cash

derivative losses, $21 million of gains from asset divestitures, a $4

million net gain on debt repurchases and a $26 million net charge from

other unusual and infrequent items.

Total daily production volumes averaged 132,000 BOE per day for the full

year of 2018 compared with 129,000 BOE per day for 2017. This net

increase included a 1,300 barrel per day negative PSC effect on

production volumes due to higher realized prices for 2018. Oil volumes

averaged 82,000 barrels per day, NGL volumes averaged 16,000 barrels per

day and gas volumes averaged 202,000 MCF per day.

Realized crude oil prices, including the effect of settled hedges,

increased $11.36 per barrel to $62.60 per barrel for the full year 2018

from $51.24 per barrel for 2017. Settled hedges reduced 2018 realized

crude oil prices by $7.51 per barrel compared with a $0.23 decrease per

barrel for 2017. Realized NGL prices increased 22% to $43.67 per barrel

for 2018 from $35.76 per barrel for 2017. Realized natural gas prices

increased 12% to $3.00 per MCF for 2018 compared with $2.67 per MCF for

2017.

Production costs for the full year of 2018 were $912 million, or $18.88

per BOE, compared to $876 million, or $18.64 per BOE, for 2017. The Elk

Hills acquisition and cash-settled stock-based compensation added $38

million and $4 million to full year production costs for 2018,

respectively. Synergies captured from the Elk Hills consolidation

reduced production costs by $17 million, partially offset by an increase

in energy costs. Per unit production costs, excluding the effect of PSC

contracts1, were $17.47 and $17.48 per BOE for the full year

of 2018 and 2017, respectively. G&A expenses were $299 million and $249

million for the full year of 2018 and 2017, respectively, with the

difference primarily related to increased equity compensation expense

resulting from CRC's higher stock price, as well as additional G&A

expense as a result of lower cost recovery following the Elk Hills

acquisition.

Taxes other than on income of $149 million for 2018 were $13 million

higher than 2017, primarily due to higher greenhouse gas (GHG) costs

related to annual price increases, in addition to a reduction in the

number of allowances granted to CRC between periods. CRC reported

exploration expenses of $34 million for the full year of 2018, or $12

million higher than 2017, due to exploration dry holes.

CRC's internally funded capital investment for 2018 totaled $641

million, of which $445 million was directed to drilling and capital

workovers. CRC's JV partner BSP funded an additional $49 million, which

is included in CRC's consolidated results, while JV partner MIRA funded

an additional $57 million of investment, which is excluded from our

consolidated results.

Cash provided by operating activities for the full year of 2018 was $461

million, which included interest payments of $441 million and $98

million of GHG payments related to prior years' allowances.

Operational Update

CRC operated an average of 10 drilling rigs during the fourth quarter of

2018 with five rigs focused on waterfloods, three on conventional

primary production, one on steamfloods and one on unconventional

production. CRC drilled 90 development wells and one exploration well

with CRC and JV capital (33 steamflood, 38 waterflood, 13 primary and 7

unconventional). Steamfloods and waterfloods have different production

profiles and longer response times than typical conventional wells and,

as a result, the full production contribution may not be experienced in

the same period that the well is drilled. In the San Joaquin basin, CRC

produced approximately 99,000 BOE per day and operated six rigs during

the fourth quarter of 2018. The Los Angeles basin contributed 26,000 BOE

per day of production and operated three rigs directed toward waterflood

projects during the fourth quarter of 2018. The Ventura basin produced

6,000 BOE per day and operated one rig directed toward waterflood

projects during the fourth quarter of 2018. The Sacramento basin

produced 5,000 BOE per day and had no active drilling program during the

fourth quarter of 2018.

2019 Capital Budget

With current oil prices slightly above $60 per barrel Brent, CRC

estimates its 2019 internally funded capital program will range from

$300 million to $385 million, which may be adjusted during the course of

the year depending on commodity prices. CRC is also in discussion to

obtain additional investments from new and existing JVs that could

increase the 2019 capital program by $100 to $150 million, to support a

total capital budget of approximately $500 million. CRC's internally

funded investments will be largely directed to quick payback projects,

such as primary drilling and capital workovers, and low-risk projects

including waterflood and steamflood investments that maintain base

production.

Balance Sheet Strengthening Update

For the fourth quarter of 2018, CRC repurchased a total of $55 million

in aggregate principal amount of CRC's outstanding debt for $50 million.

In 2018, CRC repurchased a total of $232 million in aggregate principal

amount of CRC's outstanding debt for $199 million. The majority of CRC's

debt repurchases focused on CRC's Second Lien Notes.

Year-End 2018 Reserves

CRC's proved reserves totaled 712 million barrels of oil equivalent

(MMBOE), an increase from 618 MMBOE in 2017. Excluding positive price

revisions, proved undeveloped reserves downgraded at management's

discretion and acquisitions, CRC organically replaced 127% of proved

reserves. CRC achieved this strong organic reserve replacement ratio

through well-executed capital programs in its Buena Vista, South Valley,

Huntington Beach and Long Beach areas of operations. In 2018, total

additions to proved reserves from all sources were 142 MMBOE, resulting

in an all-in reserve replacement ratio of 296%.

Hedging Update

CRC continues to opportunistically implement a hedging program to

protect its cash flow, operating margins and capital program, while

maintaining adequate liquidity. For the first and second quarters of

2019, CRC has protected the downside price risk of approximately 45,000

and 40,000 barrels per day at approximately $66 Brent and $70 Brent per

barrel, respectively. For the third and fourth quarters of 2019, CRC has

protected the downside price risk of approximately 40,000 and 35,000

barrels per day at approximately $73 Brent and $76 Brent per barrel,

respectively. Except for a small portion primarily in the first quarter

of 2019, the 2019 hedges do not contain caps, thereby providing upside

to oil price movements. See Attachment 10 for more details.

1 See Attachment 3 for how CRC calculates and uses the

non-GAAP measures of adjusted EBITDAX, core adjusted EBITDAX, adjusted

EBITDAX margin, free cash flow, production costs (excluding the effects

of PSC-type contracts) and adjusted net income (loss), and for

reconciliations of the foregoing to their nearest GAAP measure.

Conference Call Details

To participate in today's conference call scheduled for 5:00 P.M.

Eastern Standard Time, either dial (877) 328-5505 (International calls

please dial +1 (412) 317-5421) or access via webcast at www.crc.com,

fifteen minutes prior to the scheduled start time to register.

Participants may also pre-register for the conference call at http://dpregister.com/10127347.

A digital replay of the conference call will be archived for

approximately 30 days and supplemental slides for the conference call

will be available online in the Investor Relations section of www.crc.com.

About California Resources Corporation

California Resources Corporation is the largest oil and natural gas

exploration and production company in California on a gross-operated

basis. CRC operates its world-class resource base exclusively within the

State of California, applying complementary and integrated

infrastructure to gather, process and market its production. Using

advanced technology, California Resources Corporation focuses on safely

and responsibly supplying affordable energy for California by

Californians.

Forward-Looking Statements

This presentation contains forward-looking statements that involve risks

and uncertainties that could materially affect CRC's expected results of

operations, liquidity, cash flows and business prospects. Such

statements include those regarding CRC's expectations as to its future:

-

financial position, liquidity, cash flows and results of operations

-

business prospects

-

transactions and projects

-

operating costs

-

Value Creation Index (VCI) metrics, which are based on certain

estimates including future production rates, costs and commodity prices

-

operations and operational results including production, hedging and

capital investment

-

budgets and maintenance capital requirements

-

reserves

-

type curves

-

expected synergies from acquisitions and joint ventures

Actual results may differ from anticipated results, sometimes

materially, and reported results should not be considered an indication

of future performance. While CRC believes assumptions or bases

underlying its expectations are reasonable and make them in good faith,

they almost always vary from actual results, sometimes materially. CRC

also believes third-party statements it cites are accurate, but has not

independently verified them and does not warrant their accuracy or

completeness. Factors (but not necessarily all the factors) that could

cause results to differ include:

-

commodity price changes

-

debt limitations on CRC's financial flexibility

-

insufficient cash flow to fund planned investments, debt repurchases

or changes to CRC's capital plan

-

inability to enter desirable transactions, including acquisitions,

asset sales and joint ventures

-

legislative or regulatory changes, including those related to

drilling, completion, well stimulation, operation, maintenance or

abandonment of wells or facilities, managing energy, water, land,

greenhouse gases or other emissions, protection of health, safety and

the environment, or transportation, marketing and sale of our products

-

joint ventures and acquisitions and CRC's ability to achieve expected

synergies

-

the recoverability of resources and unexpected geologic conditions

-

incorrect estimates of reserves and related future cash flows and the

inability to replace reserves

-

changes in business strategy

-

PSC effects on production and unit production costs

-

effect of stock price on costs associated with incentive compensation

-

insufficient capital, including as a result of lender restrictions,

unavailability of capital markets or inability to attract potential

investors

-

effects of hedging transactions

-

equipment, service or labor price inflation or unavailability

-

availability or timing of, or conditions imposed on, permits and

approvals

-

lower-than-expected production, reserves or resources from development

projects, joint ventures or acquisitions, or higher-than-expected

decline rates

-

disruptions due to accidents, mechanical failures, transportation or

storage constraints, natural disasters, labor difficulties, cyber

attacks or other catastrophic events

-

factors discussed in "Risk Factors" in CRC's Annual Report on Form

10-K available on its website at crc.com.

Words such as "anticipate," "believe," "continue," "could," "estimate,"

"expect," "goal," "intend," "likely," "may," "might," "plan,"

"potential," "project," "seek," "should," "target, "will" or "would" and

similar words that reflect the prospective nature of events or outcomes

typically identify forward-looking statements. Any forward-looking

statement speaks only as of the date on which such statement is made and

CRC undertakes no obligation to correct or update any forward-looking

statement, whether as a result of new information, future events or

otherwise, except as required by applicable law.

|

|

|

Attachment 1

|

|

SUMMARY OF RESULTS

|

|

|

|

|

|

|

|

|

|

|

|

Fourth Quarter

|

|

Twelve Months

|

|

($ and shares in millions, except per share amounts)

|

|

2018

|

|

2017

|

|

2018

|

|

2017

|

|

|

|

|

|

|

|

|

|

|

|

Statement of Operations Data:

|

|

|

|

|

|

|

|

|

|

Revenues and Other

|

|

|

|

|

|

|

|

|

|

Oil and gas sales (a)

|

|

$

|

658

|

|

|

$

|

549

|

|

|

$

|

2,590

|

|

|

$

|

1,936

|

|

|

Net derivative gain (loss) from commodity contracts

|

|

260

|

|

|

(141

|

)

|

|

|

1

|

|

|

(90

|

)

|

|

|

Other revenue (a)

|

|

160

|

|

|

47

|

|

|

473

|

|

|

160

|

|

|

Total revenues and other

|

|

1,078

|

|

|

455

|

|

|

3,064

|

|

|

2,006

|

|

|

|

|

|

|

|

|

|

|

|

|

Costs and Other

|

|

|

|

|

|

|

|

|

|

Production costs

|

|

233

|

|

|

227

|

|

|

912

|

|

|

876

|

|

|

General and administrative expenses

|

|

65

|

|

|

66

|

|

|

299

|

|

|

249

|

|

|

Depreciation, depletion and amortization

|

|

130

|

|

|

132

|

|

|

502

|

|

|

544

|

|

|

Taxes other than on income

|

|

29

|

|

|

33

|

|

|

149

|

|

|

136

|

|

|

Exploration expense

|

|

16

|

|

|

5

|

|

|

34

|

|

|

22

|

|

|

Other expenses, net (a)

|

|

140

|

|

|

30

|

|

|

399

|

|

|

106

|

|

|

Total costs and other

|

|

613

|

|

|

493

|

|

|

2,295

|

|

|

1,933

|

|

|

|

|

|

|

|

|

|

|

|

|

Operating Income (Loss)

|

|

465

|

|

|

(38

|

)

|

|

|

769

|

|

|

73

|

|

|

|

|

|

|

|

|

|

|

|

|

Non-Operating (Loss) Income

|

|

|

|

|

|

|

|

|

|

Interest and debt expense, net

|

|

(98

|

)

|

|

|

(91

|

)

|

|

|

(379

|

)

|

|

|

(343

|

)

|

|

|

Net gain on early extinguishment of debt

|

|

31

|

|

|

—

|

|

|

57

|

|

|

4

|

|

|

Gain on asset divestitures

|

|

1

|

|

|

—

|

|

|

5

|

|

|

21

|

|

|

Other non-operating expenses

|

|

(7

|

)

|

|

|

(6

|

)

|

|

|

(23

|

)

|

|

|

(17

|

)

|

|

|

|

|

|

|

|

|

|

|

|

|

Income (Loss) Before Income Taxes

|

|

392

|

|

|

(135

|

)

|

|

|

429

|

|

|

(262

|

)

|

|

|

Income tax

|

|

—

|

|

|

—

|

|

|

—

|

|

|

—

|

|

|

Net Income (Loss)

|

|

392

|

|

|

(135

|

)

|

|

|

429

|

|

|

(262

|

)

|

|

|

Net income attributable to noncontrolling interests

|

|

(46

|

)

|

|

|

(3

|

)

|

|

|

(101

|

)

|

|

|

(4

|

)

|

|

|

Net Income (Loss) Attributable to Common Stock

|

|

$

|

346

|

|

|

$

|

(138

|

)

|

|

|

$

|

328

|

|

|

$

|

(266

|

)

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income (loss) attributable to common stock per share - basic (b)

|

|

$

|

7.00

|

|

|

$

|

(3.23

|

)

|

|

|

$

|

6.77

|

|

|

$

|

(6.26

|

)

|

|

|

Net income (loss) attributable to common stock per share - diluted

|

|

$

|

7.00

|

|

|

$

|

(3.23

|

)

|

|

|

$

|

6.77

|

|

|

$

|

(6.26

|

)

|

|

|

|

|

|

|

|

|

|

|

|

|

Adjusted net income (loss)

|

|

$

|

26

|

|

|

$

|

(14

|

)

|

|

|

$

|

61

|

|

|

$

|

(187

|

)

|

|

|

Adjusted net income (loss) per share - basic (b)

|

|

$

|

0.53

|

|

|

$

|

(0.33

|

)

|

|

|

$

|

1.27

|

|

|

$

|

(4.40

|

)

|

|

|

Adjusted net income (loss) per share - diluted

|

|

$

|

0.53

|

|

|

$

|

(0.33

|

)

|

|

|

$

|

1.27

|

|

|

$

|

(4.40

|

)

|

|

|

|

|

|

|

|

|

|

|

|

|

Weighted-average common shares outstanding - basic

|

|

$

|

48.6

|

|

|

$

|

42.7

|

|

|

$

|

47.4

|

|

|

$

|

42.5

|

|

|

Weighted-average common shares outstanding - diluted

|

|

$

|

48.6

|

|

|

$

|

42.7

|

|

|

$

|

47.4

|

|

|

$

|

42.5

|

|

|

|

|

|

|

|

|

|

|

|

|

Adjusted EBITDAX

|

|

$

|

314

|

|

|

$

|

231

|

|

|

$

|

1,117

|

|

|

$

|

779

|

|

|

Effective tax rate

|

|

0

|

%

|

|

0

|

%

|

|

0

|

%

|

|

0

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(a) We adopted a new revenue recognition standard on January 1, 2018

which required certain sales-related costs to be reported as expense

as opposed to being netted against revenue. The adoption of this

standard does not affect net income. Results for reporting periods

beginning January 1, 2018 are presented under the new accounting

standard while prior periods are not adjusted and continue to be

reported under accounting standards in effect for the applicable

period. Under prior accounting standards, for the three and twelve

months ended December 31, 2018, oil and gas sales would have been

$653 million and $2,568 million, respectively, other revenue would

have been $150 million and $392 million, respectively, and other

expenses, net would have been $125 million and $296 million,

respectively.

|

|

|

|

|

(b) In calculating Net income (loss) attributable to common stock

per share - basic, income of $6 million and $7 million for the three

and twelve months ended December 31, 2108, respectively, was

allocated to unvested participating securities with the balance of

undistributed earnings allocated to common shares. In calculating

Adjusted net income (loss) per share - basic, none and $1 million

for the three and twelve months ended December 31, 2018,

respectively, was allocated to unvested participating securities

with the balance of undistributed earnings allocated to common

shares. For periods of losses no allocation is made to participating

securities.

|

|

|

|

|

|

Fourth Quarter

|

|

Twelve Months

|

|

($ and shares in millions)

|

|

2018

|

|

2017

|

|

2018

|

|

2017

|

|

|

|

|

|

|

|

|

|

|

|

Cash Flow Data:

|

|

|

|

|

|

|

|

|

|

Net cash provided by operating activities

|

|

$

|

68

|

|

|

$

|

23

|

|

|

$

|

461

|

|

|

$

|

248

|

|

|

Net cash used in investing activities

|

|

$

|

(191

|

)

|

|

$

|

(139

|

)

|

|

$

|

(1,156

|

)

|

|

$

|

(313

|

)

|

|

Net cash provided by financing activities

|

|

$

|

109

|

|

|

$

|

108

|

|

|

$

|

692

|

|

|

$

|

73

|

|

|

|

|

|

|

|

|

|

|

|

|

Selected Balance Sheet Data:

|

|

December 31,

|

|

December 31,

|

|

|

|

|

|

|

|

2018

|

|

2017

|

|

|

|

|

|

Total current assets

|

|

$

|

640

|

|

|

$

|

483

|

|

|

|

|

|

|

Total property, plant and equipment, net

|

|

$

|

6,455

|

|

|

$

|

5,696

|

|

|

|

|

|

|

Total current liabilities

|

|

$

|

607

|

|

|

$

|

732

|

|

|

|

|

|

|

Long-term debt

|

|

$

|

5,251

|

|

|

$

|

5,306

|

|

|

|

|

|

|

Other long-term liabilities

|

|

$

|

575

|

|

|

$

|

602

|

|

|

|

|

|

|

Mezzanine equity

|

|

$

|

756

|

|

|

$

|

—

|

|

|

|

|

|

|

Equity

|

|

$

|

(247

|

)

|

|

$

|

(720

|

)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Outstanding shares as of

|

|

48.7

|

|

|

42.9

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

STOCK-BASED COMPENSATION

|

|

|

|

Our consolidated results of operations for the three and twelve

months ended December 31, 2018 include the effects of long- term

stock-based compensation plans under which we annually grant

awards to executives, non-executive employees and non-employee

directors that are either settled with shares of our common stock

or cash. Our equity-settled awards granted to executives include

stock options, restricted stock and performance stock units that

either cliff vest at the end of a three-year period or vest

ratably over a three-year period, some of which are partially

settled in cash. Our equity-settled awards granted to non-employee

directors are restricted stock units that cliff vest after one

year. Our cash-settled awards granted to non-executive employees

vest ratably over a three-year period.

|

|

|

|

Changes in our stock price introduces volatility in our income

statement because we pay partially or fully cash-settled awards

based on our stock price as of the vesting date and accounting rules

require that we adjust our obligation for such awards to the amount

that would be paid using our stock price as of the end of each

reporting period. Cash-settled awards, including executive awards

partially settled in cash, account for over 50% of our total

outstanding awards. The increase in our stock price in 2018 resulted

in higher cash-settled stock-based compensation expense in the

second and third quarters of 2018 when a portion of these awards

vested and our unvested awards were marked-to-market based on the

period-end stock price. In the fourth quarter of 2018, our stock

price declined and the year-end mark-to-market adjustments reduced

our compensation expense. Equity-settled awards are not similarly

adjusted for changes in our stock price.

|

|

|

|

Stock-based compensation is included in both general and

administrative expenses and production costs as shown in the table

below:

|

|

|

|

Fourth Quarter

|

|

Twelve Months

|

|

($ in millions, except per BOE amounts)

|

|

2018

|

|

2017

|

|

2018

|

|

2017

|

|

|

|

|

|

|

|

|

|

|

|

Expense (Income)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

General and administrative expenses

|

|

|

|

|

|

|

|

|

|

Cash-settled awards

|

|

$

|

(10

|

)

|

|

$

|

6

|

|

|

$

|

23

|

|

|

$

|

9

|

|

Equity-settled awards

|

|

2

|

|

|

3

|

|

|

13

|

|

|

14

|

|

Total stock-based compensation in G&A

|

|

$

|

(8

|

)

|

|

$

|

9

|

|

|

$

|

36

|

|

|

$

|

23

|

|

Total stock-based compensation in G&A per Boe

|

|

$

|

(0.64

|

)

|

|

$

|

0.78

|

|

|

$

|

0.75

|

|

|

$

|

0.49

|

|

|

|

|

|

|

|

|

|

|

|

Production costs

|

|

|

|

|

|

|

|

|

|

Cash-settled awards

|

|

$

|

(2

|

)

|

|

$

|

2

|

|

|

$

|

6

|

|

|

$

|

2

|

|

Equity-settled awards

|

|

—

|

|

|

—

|

|

|

3

|

|

|

4

|

|

Total stock-based compensation in production costs

|

|

$

|

(2

|

)

|

|

$

|

2

|

|

|

$

|

9

|

|

|

$

|

6

|

|

Total stock-based compensation in production costs per Boe

|

|

$

|

(0.16

|

)

|

|

$

|

0.17

|

|

|

$

|

0.19

|

|

|

$

|

0.13

|

|

|

|

|

|

|

|

|

|

|

|

Total company stock-based compensation

|

|

$

|

(10

|

)

|

|

$

|

11

|

|

|

$

|

45

|

|

|

$

|

29

|

|

Total company stock-based compensation per Boe

|

|

$

|

(0.80

|

)

|

|

$

|

0.95

|

|

|

$

|

0.94

|

|

|

$

|

0.62

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Attachment 2

|

|

PRODUCTION STATISTICS

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fourth Quarter

|

|

Twelve Months

|

|

Net Oil, NGLs and Natural Gas Production Per Day

|

|

2018

|

|

2017

|

|

2018

|

|

2017

|

|

|

|

|

|

|

|

|

|

|

|

Oil (MBbl/d)

|

|

|

|

|

|

|

|

|

|

San Joaquin Basin

|

|

56

|

|

|

50

|

|

|

53

|

|

|

52

|

|

Los Angeles Basin

|

|

26

|

|

|

26

|

|

|

25

|

|

|

27

|

|

Ventura Basin

|

|

4

|

|

|

4

|

|

|

4

|

|

|

4

|

|

Total

|

|

86

|

|

|

80

|

|

|

82

|

|

|

83

|

|

|

|

|

|

|

|

|

|

|

|

NGLs (MBbl/d)

|

|

|

|

|

|

|

|

|

|

San Joaquin Basin

|

|

15

|

|

|

15

|

|

|

15

|

|

|

15

|

|

Ventura Basin

|

|

1

|

|

|

1

|

|

|

1

|

|

|

1

|

|

Total

|

|

16

|

|

|

16

|

|

|

16

|

|

|

16

|

|

|

|

|

|

|

|

|

|

|

|

Natural Gas (MMcf/d)

|

|

|

|

|

|

|

|

|

|

San Joaquin Basin

|

|

168

|

|

|

138

|

|

|

165

|

|

|

140

|

|

Los Angeles Basin

|

|

2

|

|

|

1

|

|

|

1

|

|

|

1

|

|

Ventura Basin

|

|

7

|

|

|

7

|

|

|

7

|

|

|

8

|

|

Sacramento Basin

|

|

27

|

|

|

33

|

|

|

29

|

|

|

33

|

|

Total

|

|

204

|

|

|

179

|

|

|

202

|

|

|

182

|

|

|

|

|

|

|

|

|

|

|

|

Total Production (MBoe/d) (a)

|

|

136

|

|

|

126

|

|

|

132

|

|

|

129

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Note: MBbl/d refers to thousands of barrels per day; MMcf/d refers

to millions of cubic feet per day; MBoe/d refers to thousands of

barrels of oil equivalent per day.

|

|

|

|

|

(a) Natural gas volumes have been converted to BOE based on the

equivalence of energy content between six Mcf of natural gas and one

Bbl of oil. Barrels of oil equivalence does not necessarily result

in price equivalence.

|

|

|

|

Attachment 3

|

|

NON-GAAP FINANCIAL MEASURES AND RECONCILIATIONS

|

|

|

|

Our results of operations can include the effects of unusual,

out-of-period and infrequent transactions and events affecting

earnings that vary widely and unpredictably (in particular certain

non-cash items such as derivative gains and losses) in nature,

timing, amount and frequency. Therefore, management uses a measure

called adjusted net income (loss) which excludes those items. This

measure is not meant to disassociate items from management's

performance, but rather is meant to provide useful information to

investors interested in comparing our performance between periods.

Reported earnings are considered representative of management's

performance over the long term. Adjusted net income (loss) is not

considered to be an alternative to net income (loss) reported in

accordance with U.S. generally accepted accounting principles (GAAP).

|

|

|

|

We define certain of our non-GAAP financial measures as follows:

|

|

|

|

(1) Adjusted EBITDAX is calculated as earnings before interest

expense; income taxes; depreciation, depletion and amortization;

exploration expense; other unusual, out-of-period and infrequent

items; and other non-cash items.

|

|

|

|

(2) Core Adjusted EBITDAX removes the transitory effects of settled

hedges and cash-settled stock-based compensation expense from

Adjusted EBITDAX.

|

|

|

|

(3) Free Cash Flow is net cash provided by operating activities

after our internal capital investment.

|

|

|

|

(4) Discretionary Cash Flow is the cash available after payments to

our noncontrolling interest holders and cash interest, excluding the

effect of working capital changes but before our internal capital

investment.

|

|

|

|

We believe these measures provide useful information in assessing

our financial condition, results of operations and cash flows and

are widely used by the industry, the investment community and our

lenders. Although these are non-GAAP measures, the amounts included

in the calculations were computed in accordance with GAAP. Certain

items excluded from these non-GAAP measures are significant

components in understanding and assessing our financial performance,

such as our cost of capital and tax structure, as well as the

historic cost of depreciable and depletable assets. These measures

should be read in conjunction with the information contained in our

financial statements prepared in accordance with GAAP. A version of

Adjusted EBITDAX is a material component of certain of our financial

covenants under our 2014 Revolving Credit Facility and is provided

in addition to, and not as an alternative for, income and liquidity

measures calculated in accordance with GAAP.

|

|

|

|

|

|

ADJUSTED NET INCOME (LOSS)

|

|

|

|

The following table presents a reconciliation of the GAAP financial

measure of net income (loss) attributable to common stock to the

non-GAAP financial measure of adjusted net income (loss) and

presents the GAAP financial measure of net income (loss)

attributable to common stock per diluted share and the non-GAAP

financial measure of adjusted net income (loss) per diluted share:

|

|

|

|

|

|

|

|

|

|

Fourth Quarter

|

|

Twelve Months

|

|

($ millions, except per share amounts)

|

|

2018

|

|

2017

|

|

2018

|

|

2017

|

|

Net income (loss)

|

|

$

|

392

|

|

|

$

|

(135

|

)

|

|

$

|

429

|

|

|

$

|

(262

|

)

|

|

Net income attributable to noncontrolling interests

|

|

(46

|

)

|

|

(3

|

)

|

|

(101

|

)

|

|

(4

|

)

|

|

Net income (loss) attributable to common stock

|

|

346

|

|

|

(138

|

)

|

|

328

|

|

|

(266

|

)

|

|

Unusual, infrequent and other items:

|

|

|

|

|

|

|

|

|

|

Non-cash derivative (gain) loss from commodities excluding

noncontrolling interest

|

|

(295

|

)

|

|

116

|

|

|

(224

|

)

|

|

78

|

|

|

Non-cash derivative loss from interest-rate contracts

|

|

6

|

|

|

—

|

|

|

6

|

|

|

—

|

|

|

Early retirement and severance costs

|

|

—

|

|

|

1

|

|

|

4

|

|

|

5

|

|

|

Gain on asset divestitures

|

|

(1

|

)

|

|

—

|

|

|

(5

|

)

|

|

(21

|

)

|

|

Net gain on early extinguishment of debt

|

|

(31

|

)

|

|

—

|

|

|

(57

|

)

|

|

(4

|

)

|

|

Other, net

|

|

1

|

|

|

7

|

|

|

9

|

|

|

21

|

|

|

Total unusual, infrequent and other items

|

|

(320

|

)

|

|

124

|

|

|

(267

|

)

|

|

79

|

|

|

|

|

|

|

|

|

|

|

|

|

Adjusted net income (loss)

|

|

$

|

26

|

|

|

$

|

(14

|

)

|

|

$

|

61

|

|

|

$

|

(187

|

)

|

|

|

|

|

|

|

|

|

|

|

|

Net income (loss) attributable to common stock per share - diluted

|

|

$

|

7.00

|

|

|

$

|

(3.23

|

)

|

|

$

|

6.77

|

|

|

$

|

(6.26

|

)

|

|

Adjusted net income (loss) per share - diluted

|

|

$

|

0.53

|

|

|

$

|

(0.33

|

)

|

|

$

|

1.27

|

|

|

$

|

(4.40

|

)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

DERIVATIVE GAINS AND LOSSES

|

|

|

|

|

|

|

|

Fourth Quarter

|

|

Twelve Months

|

|

($ millions)

|

|

2018

|

|

2017

|

|

2018

|

|

2017

|

|

Commodity Contracts:

|

|

|

|

|

|

|

|

|

|

Non-cash derivative gain (loss) excluding noncontrolling interest

|

|

$

|

295

|

|

|

$

|

(116

|

)

|

|

$

|

224

|

|

|

$

|

(78

|

)

|

|

Non-cash derivative gain (loss) included in noncontrolling interest

|

|

15

|

|

|

(3

|

)

|

|

5

|

|

|

(5

|

)

|

|

Net payments on settled commodity derivatives

|

|

(50

|

)

|

|

(22

|

)

|

|

(228

|

)

|

|

(7

|

)

|

|

Net derivative gain (loss) from commodity contracts

|

|

$

|

260

|

|

|

$

|

(141

|

)

|

|

$

|

1

|

|

|

$

|

(90

|

)

|

|

|

|

|

|

|

|

|

|

|

|

Interest Rate Contracts:

|

|

|

|

|

|

|

|

|

|

Non-cash derivative loss

|

|

$

|

(6

|

)

|

|

$

|

—

|

|

|

$

|

(6

|

)

|

|

$

|

—

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FREE CASH FLOW

|

|

|

|

|

|

|

|

|

|

|

|

Fourth Quarter

|

|

Twelve Months

|

|

($ millions)

|

|

2018

|

|

2017

|

|

2018

|

|

2017

|

|

|

|

|

|

|

|

|

|

|

|

Net cash provided by operating activities

|

|

$

|

68

|

|

|

$

|

23

|

|

|

$

|

461

|

|

|

$

|

248

|

|

|

Capital investment

|

|

(186

|

)

|

|

(139

|

)

|

|

(690

|

)

|

|

(371

|

)

|

|

Free cash flow

|

|

(118

|

)

|

|

(116

|

)

|

|

(229

|

)

|

|

(123

|

)

|

|

BSP funded capital investment

|

|

12

|

|

|

14

|

|

|

49

|

|

|

96

|

|

|

Free cash flow excluding BSP funded capital

|

|

$

|

(106

|

)

|

|

$

|

(102

|

)

|

|

$

|

(180

|

)

|

|

$

|

(27

|

)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

DISCRETIONARY CASH FLOW

|

|

|

|

|

|

|

|

|

|

|

|

Fourth Quarter

|

|

Twelve Months

|

|

($ millions)

|

|

2018

|

|

2017

|

|

2018

|

|

2017

|

|

Adjusted EBITDAX

|

|

$

|

314

|

|

|

$

|

231

|

|

|

$

|

1,117

|

|

|

$

|

779

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash Interest

|

|

(157

|

)

|

|

(145

|

)

|

|

(441

|

)

|

|

(396

|

)

|

|

Distributions to noncontrolling interest holders:

|

|

|

|

|

|

|

|

|

|

BSP joint venture

|

|

(21

|

)

|

|

(2

|

)

|

|

(56

|

)

|

|

(8

|

)

|

|

Ares joint venture

|

|

(20

|

)

|

|

—

|

|

|

(65

|

)

|

|

—

|

|

|

|

|

|

|

|

|

|

|

|

|

Discretionary Cash Flow

|

|

$

|

116

|

|

|

$

|

84

|

|

|

$

|

555

|

|

|

$

|

375

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ADJUSTED EBITDAX AND CORE ADJUSTED EBITDAX

|

|

|

|

The following tables present a reconciliation of the GAAP financial

measures of net income (loss) and net cash provided (used) by

operating activities to the non-GAAP financial measures of adjusted

and core adjusted EBITDAX.

|

|

|

|

|

|

|

|

|

|

Fourth Quarter

|

|

Twelve Months

|

|

($ millions)

|

|

2018

|

|

2017

|

|

2018

|

|

2017

|

|

Net income (loss)

|

|

$

|

392

|

|

|

$

|

(135

|

)

|

|

$

|

429

|

|

|

$

|

(262

|

)

|

|

Interest and debt expense, net

|

|

98

|

|

|

91

|

|

|

379

|

|

|

343

|

|

|

Depreciation, depletion and amortization

|

|

130

|

|

|

132

|

|

|

502

|

|

|

544

|

|

|

Exploration expense

|

|

16

|

|

|

5

|

|

|

34

|

|

|

22

|

|

|

Unusual, infrequent and other items (a)

|

|

(320

|

)

|

|

124

|

|

|

(267

|

)

|

|

79

|

|

|

Other non-cash items

|

|

(2

|

)

|

|

14

|

|

|

40

|

|

|

53

|

|

|

Adjusted EBITDAX

|

|

$

|

314

|

|

|

$

|

231

|

|

|

$

|

1,117

|

|

|

$

|

779

|

|

|

Net payments on settled commodity derivatives

|

|

50

|

|

|

22

|

|

|

228

|

|

|

7

|

|

|

Cash-settled stock-based compensation

|

|

(12

|

)

|

|

8

|

|

|

29

|

|

|

11

|

|

|

Core Adjusted EBITDAX

|

|

$

|

352

|

|

|

$

|

261

|

|

|

$

|

1,374

|

|

|

$

|

797

|

|

|

|

|

|

|

|

|

|

|

|

|

Net cash provided by operating activities

|

|

$

|

68

|

|

|

$

|

23

|

|

|

$

|

461

|

|

|

$

|

248

|

|

|

Cash interest

|

|

157

|

|

|

145

|

|

|

441

|

|

|

396

|

|

|

Exploration expenditures

|

|

3

|

|

|

4

|

|

|

17

|

|

|

20

|

|

|

Working capital changes

|

|

86

|

|

|

52

|

|

|

199

|

|

|

94

|

|

|

Other, net

|

|

—

|

|

|

7

|

|

|

(1

|

)

|

|

21

|

|

|

Adjusted EBITDAX

|

|

$

|

314

|

|

|

$

|

231

|

|

|

$

|

1,117

|

|

|

$

|

779

|

|

|

Net payments on settled commodity derivatives

|

|

50

|

|

|

22

|

|

|

228

|

|

|

7

|

|

|

Cash-settled stock-based compensation

|

|

(12

|

)

|

|

8

|

|

|

29

|

|

|

11

|

|

|

Core Adjusted EBITDAX

|

|

$

|

352

|

|

|

$

|

261

|

|

|

$

|

1,374

|

|

|

$

|

797

|

|

|

|

|

|

|

|

|

|

|

|

|

(a) See Adjusted Net Income (Loss) reconciliation.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ADJUSTED EBITDAX MARGIN

|

|

|

|

|

|

|

|

Fourth Quarter

|

|

Twelve Months

|

|

($ millions)

|

|

2018

|

|

2017

|

|

2018

|

|

2017

|

|

Total revenues and other

|

|

$

|

1,078

|

|

|

$

|

455

|

|

|

$

|

3,064

|

|

|

$

|

2,006

|

|

|

Non-cash derivative (gain) loss

|

|

(310

|

)

|

|

119

|

|

|

(229

|

)

|

|

83

|

|

|

Adjusted revenues

|

|

$

|

768

|

|

|

$

|

574

|

|

|

$

|

2,835

|

|

|

$

|

2,089

|

|

|

Adjusted EBITDAX Margin (b)

|

|

41

|

%

|

|

40

|

%

|

|

39

|

%

|

|

37

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(b) See Note (a) on Attachment 1 related to our adoption of a new

revenue recognition standard for the reporting of certain

sales-related costs. Under prior accounting standards, for the three

and twelve months ended December 31, 2018, the adjusted EBITDAX

margin would have been 42% and 41% respectively.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PRODUCTION COSTS PER BOE

|

|

|

|

|

|

|

|

|

|

|

|

Fourth Quarter

|

|

Twelve Months

|

|

($ per Boe)

|

|

2018

|

|

2017

|

|

2018

|

|

2017

|

|

Production costs

|

|

$

|

18.61

|

|

|

$

|

19.64

|

|

|

$

|

18.88

|

|

|

$

|

18.64

|

|

|

Excess costs attributable to PSC-type contracts

|

|

(1.17

|

)

|

|

(1.33

|

)

|

|

(1.41

|

)

|

|

(1.16

|

)

|

|

Production costs, excluding effects of PSC-type contracts

|

|

$

|

17.44

|

|

|

$

|

18.31

|

|

|

$

|

17.47

|

|

|

$

|

17.48

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PV-10 AND STANDARDIZED MEASURE

|

|

|

The following table presents a reconciliation of the GAAP financial

measure of standardized measure of discounted future net cash flows

to the non-GAAP financial measure of PV-10:

|

|

($ millions)

|

|

|

|

|

|

2018

|

|

Standardized measure of discounted future net cash flows

|

|

|

|

$

|

7,275

|

|

Present value of future income taxes discounted at 10%

|

|

|

|

2,136

|

|

PV-10 of proved reserves (1)

|

|

|

|

|

|

$

|

9,411

|

|

|

|

|

|

|

|

|

|

|

(1) PV-10 is a non-GAAP financial measure and represents the

year-end present value of estimated future cash inflows from proved

oil and natural gas reserves, less future development and production

costs, discounted at 10% per annum to reflect the timing of future

cash flows and using SEC prescribed pricing assumptions for the

period. PV-10 differs from Standardized Measure because Standardized

Measure includes the effects of future income taxes on future net

cash flows. Neither PV-10 nor Standardized Measure should be

construed as the fair value of our oil and natural gas reserves.

Standard Measure is prescribed by the SEC as an industry standard

asset value measure to compare reserves with consistent pricing,

costs and discount assumptions. PV-10 facilitates the comparisons to

other companies as it is not dependent on the tax-paying status of

the entity.

|

|

|

|

|

|

Attachment 4

|

|

|

|

|

Reserve Replacement Ratios (1)

|

|

|

|

|

|

2018

|

|

Organic Reserve Replacement Ratio (2)

|

|

|

|

|

|

|

|

|

Extensions and discoveries

|

|

|

|

|

|

30

|

|

|

Improved recovery

|

|

|

|

|

|

4

|

|

|

Revisions related to performance (excluding discretionary PUD

downgrades)

|

|

27

|

|

|

Organic proved reserves added - MMBOE (A)

|

|

|

|

|

|

61

|

|

|

|

|

|

|

|

|

|

|

|

Production in 2018 - MMBOE (B)

|

|

|

|

|

|

48

|

|

|

Organic reserve replacement ratio (A)/(B)

|

|

|

|

|

|

127

|

%

|

|

|

|

|

|

|

|

|

|

|

All-in Reserve Replacement Ratio (3)

|

|

|

|

|

|

|

|

|

Extensions and discoveries

|

|

|

|

|

|

30

|

|

|

Improved recovery

|

|

|

|

|

|

4

|

|

|

Purchases of proved reserves

|

|

|

|

|

|

64

|

|

|

Revisions related to performance

|

|

|

|

|

|

6

|

|

|

Revisions related to price

|

|

|

|

|

|

38

|

|

|

All-in proved reserves added - MMBOE (C)

|

|

|

|

|

|

142

|

|

|

|

|

|

|

|

|

|

|

|

Production in 2018 - MMBOE (D)

|

|

|

|

|

|

48

|

|

|

All-in reserve replacement ratio (C)/(D)

|

|

|

|

|

|

296

|

%

|

|

|

|

|

|

|

|

|

|

|

(1) The reserve replacement ratio is a non-GAAP measure that

management uses to gauge the results of its capital program. There

is no guarantee that historical sources of reserve additions will

continue as many factors fully or partially outside management's

control, including commodity prices, availability of capital and the

underlying geology, affect reserves additions. Other oil and gas

producers may use different methods to calculate replacement ratios,

which may affect comparability.

|

|

|

|

|

(2) The organic reserve replacement ratio is calculated for a

specified period using the proved oil-equivalent additions from

extensions and discoveries, improved recovery and

performance-related revisions (excluding 21 MMBOE of proved

undeveloped reserves downgraded at management's discretion), divided

by oil-equivalent production.

|

|

|

|

|

(3) The all-in reserve replacement ratio is calculated for a

specified period using the proved oil-equivalent additions from

extensions and discoveries, improved recovery, revisions and

purchases, divided by oil-equivalent production.

|

|

|

|

Finding and Development Costs(4)

|

|

|

|

|

|

2018

|

|

|

Exploration and development costs - in millions (A)

|

|

$

|

690

|

|

|

|

Property acquisition costs - in millions

|

|

554

|

|

|

|

Total costs incurred - in millions (B)

|

|

$

|

1,244

|

|

|

|

|

|

|

|

|

Organic proved reserves added - MMBOE (C)

|

|

61

|

|

|

|

Organic finding and development costs - $/BOE (A)/(C)

|

|

$

|

11.31

|

|

(5)

|

|

|

|

|

|

|

|

|

|

|

Total reserve replacements - MMBOE (D)

|

|

142

|

|

|

|

All-in finding and development costs - $/BOE (B)/(D)

|

|

|

|

|

|

$

|

8.76

|

|

(6)

|

|

|

|

|

|

|

|

|

|

|

|

|

(4) We believe that reporting our finding and development costs can

aid investors in their evaluation of our ability to add proved

reserves at a reasonable cost but is not a substitute for required

GAAP disclosures. Various factors, primarily timing differences and

effects of commodity price changes, can cause finding and

development costs associated with a particular period's reserves

additions to be imprecise. For example, we will need to make more

investments in order to develop the proved undeveloped reserves

added during the year and any future revisions may change the actual

measure from that presented above. In addition, part of the 2018

costs were incurred to convert proved undeveloped reserves from

prior years to proved developed reserves. In our calculations, we

have not estimated future costs to develop proved undeveloped

reserves added in 2018 or removed costs related to proved

undeveloped reserves added in prior periods. Our calculations of

finding and development costs may not be comparable to similar

measures provided by other companies.

|

|

|

|

|

(5) We calculate organic finding and development costs by dividing

the costs incurred for the year from the capital program by the

amount of oil-equivalent proved reserves added in the same year from

improved recovery, extensions and discoveries and

performance-related revisions (excluding 21 MMBOE of proved

undeveloped reserves downgraded at management's discretion).

|

|

|

|

|

(6) We calculate all-in finding and development costs by dividing