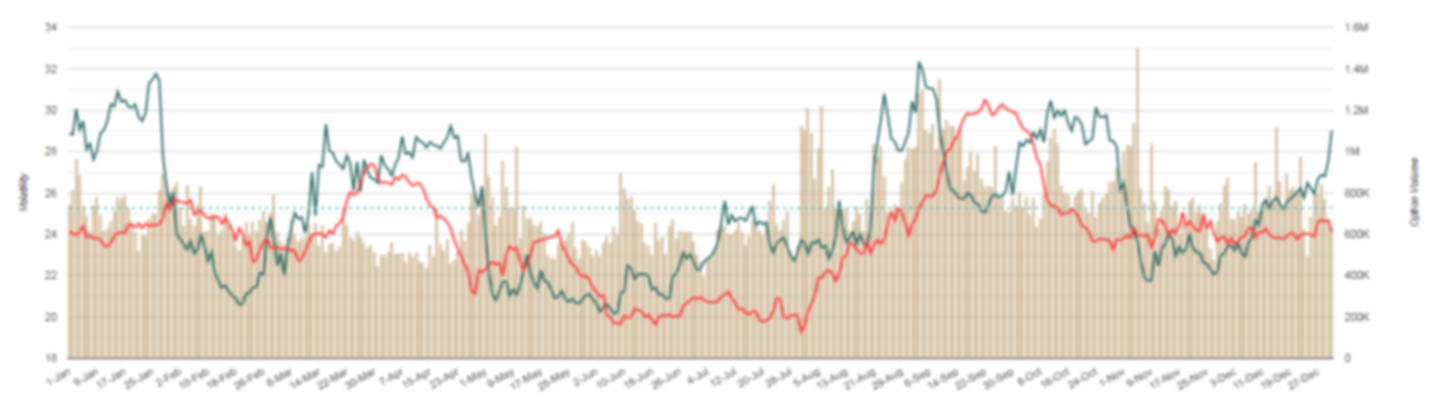

The following chart shows how implied volatility (IV30) trended by calendar period to detect seasonal patterns during the year.

Full Data Set is Available for Premium Subscribers

Login Or Try

7-Day Free Trial